The Debt Avalanche vs. Debt Snowball Method: Which One Actually Saves You More

An honest, number-driven comparison of the two most popular debt payoff strategies — showing exactly how much each costs, how long each takes, and which type of person is better suited to each method.

Two friends, same $18,000 in total debt across three accounts, same monthly payment budget. One chose the debt avalanche method and paid $1,340 in total interest over 28 months. The other chose the debt snowball and paid $1,820 in interest over 31 months. The avalanche winner saved $480 and three months of payments. The snowball person, however, had cancelled their credit card and was still on track by month six when the other had quietly stopped making extra payments altogether. The math said one thing. Human behaviour said another.

This guide settles the debt avalanche vs. debt snowball debate honestly — with real numbers, real psychology, and a clear verdict on which debt payoff strategy suits which type of person.

What Each Method Actually Is

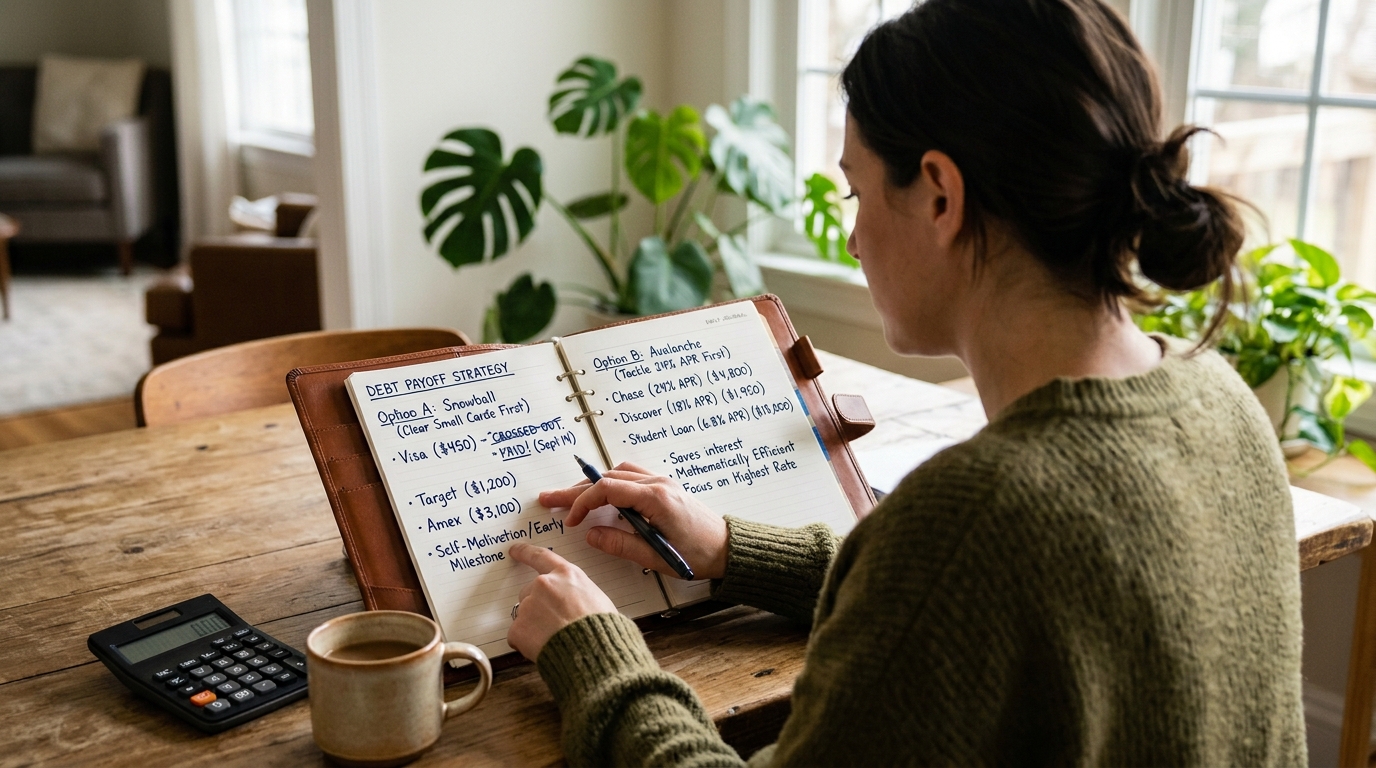

The Debt Avalanche targets the highest interest rate debt first, regardless of balance size. You make minimum payments on all other debts and direct every extra dollar at the account costing you the most in interest. Once that is cleared, you redirect the full payment to the next highest-rate debt — and so on until all debts are gone.

The Debt Snowball targets the smallest balance first, regardless of interest rate. You pay minimum payments everywhere else and throw every extra dollar at the smallest debt. When it is cleared, you roll that full payment into the next smallest balance. The name comes from the snowball effect: each cleared debt increases the payment available for the next.

Both methods use the same total monthly payment. The only difference is the order in which individual debts are eliminated. That ordering difference produces meaningfully different outcomes in both total cost and psychological experience.

The Math: Side-by-Side Comparison

Using a realistic three-debt scenario: Credit Card A ($3,500 at 22% APR), Personal Loan ($8,000 at 12% APR), Credit Card B ($6,500 at 19% APR). Total debt: $18,000. Available extra payment beyond minimums: $300 per month [SOURCE: verify with a debt payoff calculator].

In this scenario the order happens to be similar because the smallest balance (Card A at $3,500) also carries the highest interest rate (22%). When the smallest balance and the highest rate coincide on the same account, the two methods produce identical results. The divergence appears when the smallest balance carries a low rate and the largest carries a high one.

A more revealing scenario: Credit Card A ($1,200 at 8% APR — the smallest balance), Personal Loan ($8,500 at 14% APR), Credit Card B ($8,300 at 24% APR — the highest rate). Here the avalanche attacks the 24% card immediately; the snowball clears the $1,200 balance first and gets to the 24% card months later. The interest difference in this scenario can exceed $900 over the repayment period [SOURCE: verify].

The Psychology: Why the Snowball Has a Real Advantage

The avalanche method is mathematically optimal. That optimality is irrelevant if you quit on month three — and research on debt repayment behaviour suggests that early wins measurably improve the probability of sustained effort [SOURCE: verify — Kellogg School debt payoff motivation research].

What most debt guides won't tell you: the motivational effect of eliminating an entire account is disproportionate to its financial impact. Closing an account — regardless of balance — produces a concrete, visible win. The number of open debt accounts decreases. The mental load lightens. The sense of progress is real and immediate.

The avalanche method can run for many months before the first account closes, particularly if the highest-rate debt also carries a large balance. For people who need the psychological reward of a cleared account to maintain motivation — which is most people — this extended period without visible progress is where the method most commonly breaks down.

Hypothetical example: Kwame has four debts ranging from $800 to $9,000. He starts the avalanche method, correctly targeting his 23% APR card. That card has a $7,200 balance. Fourteen months later, having made every payment, he has reduced it to $3,900 — but still has four open accounts. His motivation has eroded significantly. He could have cleared his $800 and $1,400 debts in the same period using the snowball and would now have two fewer accounts and significantly stronger resolve to continue. The interest cost difference between the methods: approximately $340. The adherence cost of choosing the wrong method for his psychology: potentially the entire repayment plan.

Which Method Is Right for You

The honest answer depends on one question: are you more motivated by mathematical efficiency or by visible progress milestones?

Choose the Debt Avalanche if: You are disciplined about tracking numbers, you will not lose motivation during a long stretch without a full account closure, you have high-interest debt that significantly diverges from low-interest debt in rate (making the interest savings substantial), and you are primarily motivated by optimising the total cost.

Choose the Debt Snowball if: You have tried debt repayment plans before and lost momentum, you have several small balances that can be cleared quickly, you are more motivated by reducing the number of open accounts than by minimising interest, and the difference in interest cost between the two methods in your specific situation is modest.

A common mistake I have seen: people choose the avalanche because it is the 'smart' method, make excellent early progress, then quietly revert to minimum payments after six months because nothing has visibly changed. A completed snowball plan at slightly higher cost beats an abandoned avalanche plan at every income level.

Disclaimer: This article is for informational purposes only and does not constitute professional financial advice. Consult a qualified financial advisor for guidance specific to your situation.

A Hybrid Approach That Works for Many People

If you have one or two very small balances (under $500) alongside larger high-interest debts, consider a brief hybrid: clear the small balances immediately for the motivational win, then switch to strict avalanche order for all remaining debts. The interest cost of clearing a $400 balance at 8% before attacking a $6,000 balance at 22% is minimal — typically under $50 over the full repayment period — while the psychological benefit of eliminating accounts early is real and measurable.

Key Takeaways

- The debt avalanche (highest interest first) saves more money mathematically — the savings range from modest to significant depending on the interest rate gap between debts

- The debt snowball (smallest balance first) produces earlier visible wins that improve adherence — and a plan you complete always beats one you abandon

- When the smallest balance and highest interest rate belong to the same debt, both methods are identical

- Choose based on your specific motivational pattern, not on which sounds more financially sophisticated

- A hybrid approach — clearing small balances first, then switching to avalanche order — balances both at minimal extra cost

Frequently Asked Questions

Which method saves more money overall?

The debt avalanche always saves equal or more money than the debt snowball, because it minimises the time high-interest balances remain unpaid. The size of the saving depends on the interest rate difference between your debts. If your rates are similar, the saving is small. If you have a 25% APR card alongside a 6% loan, the avalanche saves meaningfully more over the full repayment period.

Does the debt snowball actually work?

Yes — and research supports it. Studies on consumer debt repayment behaviour find that people who clear individual accounts early are more likely to continue and complete their repayment plan than those who do not experience early wins. For many people, the motivational benefit of the snowball produces a better real-world outcome than the mathematical efficiency of the avalanche — because they actually finish.

Can I switch methods midway through?

Yes, and it is sometimes the right move. If you started with the avalanche and motivation is flagging, switching to clear one or two smaller accounts can restore momentum without catastrophically increasing your total interest cost. The most important thing is maintaining consistent extra payments — the method is less important than the commitment to continuing.

Should I include my mortgage in either method?

Most people exclude the mortgage from these methods and focus on consumer debt: credit cards, personal loans, car finance, and student loans. Mortgages typically carry lower rates than consumer debt and have tax implications that vary by country. Address high-interest consumer debt first; revisit mortgage overpayment strategy separately with appropriate financial advice for your jurisdiction.

What if I can only afford minimum payments right now?

Neither method works without an extra payment above the minimums. If your budget genuinely only covers minimums, the priority is creating any additional cash flow — reducing discretionary spending, adding income, or contacting creditors about hardship arrangements. Even $30 extra per month applied to one debt makes a measurable difference over time and gets the system moving.