The 50/30/20 Budget Rule: Does It Actually Work in 2026?

An honest, data-informed evaluation of the 50/30/20 budget rule — where it works, where it breaks down for modern incomes and housing costs, and what to do when the numbers do not add up.

Most budgeting advice is written by people who can afford to follow it. The 50/30/20 budget rule is no exception. It is clean, intuitive, and works perfectly for the income level its author had in mind when she wrote it in 2005. If your rent is $1,800 and your take-home is $3,200, the rule does not give you a budget. It gives you a deficit with a name.

When Elizabeth Warren first outlined the 50/30/20 budget rule, the average American renter spent roughly 28-30% of income on housing. Today, in cities like New York, London, Sydney, and Toronto, that figure routinely exceeds 40-50% for median earners. The rule has not been updated. The cost of living has.

This article does not just explain the 50/30/20 budget rule in 2026. It stress-tests it honestly, across income levels and life situations, and tells you what to do when the numbers do not cooperate.

What the 50/30/20 Rule Actually Says

The rule is straightforward: allocate 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. Needs means the non-negotiables: rent or mortgage, utilities, groceries, transportation, insurance, and minimum debt payments. Wants covers everything discretionary. Savings includes emergency funds, retirement contributions, and any extra debt repayment beyond the minimum.

The line between needs and wants is where people immediately run into trouble (and where most budgeting arguments between partners start — one person's need is the other's obvious want). The rule does not answer these questions — it just gives you a bucket and a percentage, and expects you to figure out the contents.

The Case For It — Why the Rule Has Survived 20 Years

Budgeting systems fail mostly because people abandon them. Complexity is the primary cause of abandonment. On that measure, the 50/30/20 rule has a genuine advantage — it reduces a month of financial decisions to three numbers.

For the right person in the right circumstances, it works exactly as intended. Hypothetical example: Jamie is 32, a teacher in a mid-sized US city, earning $52,000 a year. Monthly take-home after taxes: approximately $3,500. Her rent is $980, utilities average $130, groceries run $350, and her car costs $280 per month. Total needs: $1,740. The rule fits with $10 to spare. Her 20% savings goes to a retirement account and an emergency fund. The 30% wants cover weekend plans and the occasional trip.

Jamie's situation is not unusual — it is just also not New York, London, or Vancouver. Change the housing market or add student loan debt and the 50/30/20 budget rule starts to strain immediately.

Where the 50/30/20 Rule Breaks Down in 2026

Three forces have quietly dismantled the conditions that made the rule functional for average earners:

1. Housing costs have outpaced the math. In 2026, the median rent for a one-bedroom apartment in major English-speaking cities runs $1,800-$2,800 per month [SOURCE: verify — Zillow, Rightmove, Domain AU]. For someone earning $55,000 a year with a $3,600 monthly take-home, that is 50-78% of income before a single utility, grocery, or transport cost.

2. Student loan debt has restructured the savings bucket. The average US graduate carries approximately $37,000 in student loan debt [SOURCE: verify — Federal Reserve or NCES data]. Monthly loan payments alone consume a significant portion of the 20% savings allocation, often leaving nothing for emergency funds or retirement.

3. Inflation has expanded the definition of needs. Between 2021 and 2026, grocery costs, insurance premiums, energy bills, and healthcare costs have risen at rates consistently above wage growth [SOURCE: verify — CPI data]. Needs that once consumed 40% of a moderate income now routinely push 55-60%.

The 50/30/20 Rule Across Income Levels — A Reality Check

The pattern is clear: the 50/30/20 budget rule in 2026 is functionally a middle-to-upper-middle income framework. Below roughly $4,000 monthly take-home in an urban environment, the needs bucket expands beyond 50% almost automatically — not through poor choices, but through the arithmetic of fixed costs in a high-inflation, high-rent market.

The Contrarian Case — When Following 50/30/20 Is the Wrong Move

Rigidly following the 50/30/20 rule can actively hurt your financial progress in certain situations.

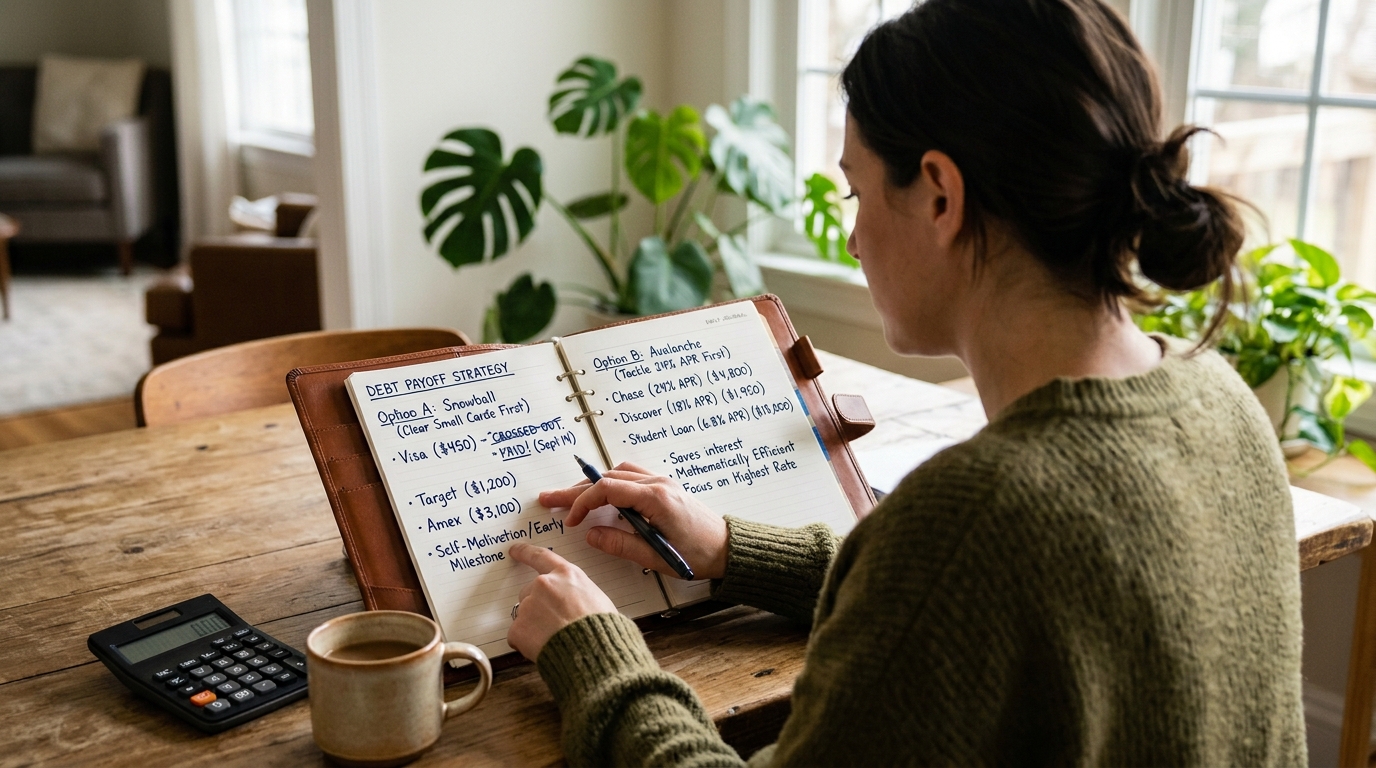

If you carry high-interest debt: A common mistake — people open a high-yield savings account earning 4.5% interest while carrying a credit card balance at 22% APR, because the rule told them to save 20%. That is not financial discipline — it is paying a bank to feel responsible. Clear the high-interest debt first. Every dollar saved in a 4% account while paying 24% APR on a credit card costs you money. The 20% savings bucket should be redirected almost entirely to debt elimination — temporarily running something closer to a 50/10/40 split until the obligation is cleared.

If your income is irregular: Freelancers and commission-based earners receive income in lumps, not smooth monthly streams. Applying fixed percentages to variable income creates a different calculation every month. A better approach: calculate your needs in absolute dollars, set that as your floor, and direct everything above it to savings first during high-income months as a buffer against lean months.

If you are below the income floor where the rule functions: Forcing a 50/30/20 split on $28,000 annual income in a city where rent averages $1,200 does not produce a budget — it produces a deficit. Zero-based budgeting, where you assign every dollar a specific job starting from actual expenses, is more useful below this threshold than any percentage rule.

Disclaimer: This article is for informational purposes only and does not constitute professional financial advice. Consult a qualified financial advisor before making significant changes to your financial strategy.

How to Adapt the 50/30/20 Rule for 2026 Realities

The 60/20/20 adjustment for high-cost areas: Accept that housing and basic costs will eat 60% and move the pressure to the wants bucket, not the savings bucket. Compress discretionary spending to 20%, hold savings at 20%. The savings rate does not drop — the lifestyle budget absorbs the pressure.

The debt-first modification: Temporarily run 50/40/10, with the extra 10% redirected from wants to high-interest debt repayment. Once cleared, rebuild the savings allocation to the full 20%.

The income-scaling approach: Rather than percentage targets, set a fixed monthly savings dollar amount based on your actual goals — emergency fund target, retirement contribution, specific purchase — and treat that amount as a non-negotiable expense. What remains is what you have to work with.

Hypothetical example: Priya is a 29-year-old marketing manager in London earning the equivalent of approximately $3,300 per month take-home. Her rent is $1,760 — 53% of take-home before any other expense. A strict 50/30/20 split is structurally impossible. Instead she runs 58/22/20 — accepting that needs eat 58%, compressing discretionary spending to 22%, and protecting her 20% savings rate by automating the transfer on payday. The percentages are wrong by the book. The outcome — consistent saving, clear spending awareness — is right.

The Right Way to Think About Budget Rules

What most budgeting guides skip is this: the 50/30/20 rule does not fail because people are undisciplined. It fails because fixed percentages applied to a variable cost structure produce different results at every income level — and nobody tells you which income level the rule was calibrated for.

The only number that actually predicts long-term financial health is your savings rate — what percentage of income you consistently set aside over years, not the specific category split that gets you there. Any budget you can follow beats a perfect budget you abandon after two weeks.

Key Takeaways

- The 50/30/20 rule was designed for a specific income level and cost-of-living environment that no longer describes most urban earners in 2026

- It works well for mid-to-upper-middle incomes in moderate-cost cities — and breaks down quickly outside those conditions

- High housing costs, student loan debt, and inflation have each expanded the needs bucket beyond the 50% target for millions of people

- Adapt the percentages: 60/20/20 for high-cost cities, 50/40/10 temporarily for debt payoff, zero-based budgeting below the income floor

- The rule's underlying principle — separate needs from wants, pay yourself first — remains valid even when the exact percentages do not apply

Frequently Asked Questions

Is the 50/30/20 rule still relevant in 2026?

It remains a useful starting framework but its specific percentages work best for middle incomes in moderate-cost areas. In high-rent cities or for people carrying significant debt, the 50% needs allocation is often structurally impossible. The principle matters more than the percentages: track spending by category and consistently prioritise savings.

What counts as a need in the 50/30/20 budget?

Needs are fixed, non-negotiable expenses: rent or mortgage, utilities, basic groceries, transportation required for work, insurance, and minimum debt payments. The boundary gets blurry with items like gym memberships and phone plans — classify honestly based on whether going without would cause genuine functional harm, not merely discomfort.

What should I do if my rent is more than 50% of my income?

Adjust the percentages rather than misclassify your expenses. A 60/20/20 or even 65/15/20 split — compressing discretionary spending while protecting the savings rate — is more honest and more functional than pretending your rent is lower than it is. Longer term, explore income growth, relocation, or shared living to rebalance the equation.

Is 20% savings realistic on a low income?

Below a certain income floor, no. A better target: save any consistent amount, even 1-5%, and build the habit. As income grows, scale the savings rate. One concrete dollar saved automatically is more valuable than a 20% aspiration that never happens. Zero-based budgeting tends to serve lower incomes better than percentage frameworks.

What is a better alternative to the 50/30/20 rule?

For high earners: the 80/20 rule — save 20% first and spend the rest however you choose, without category tracking. For debt holders: avalanche or snowball method prioritising debt first. For low incomes or complex situations: zero-based budgeting, where every dollar is assigned a specific purpose each month.